Hub and spoke versus direct services in container shipping: an analysis

The Red Sea crisis has prompted shipping lines to re-consider the hub and spoke strategy and increase their direct services allowing the carriers to absorb excess capacity and reduce their vulnerability to port congestion.

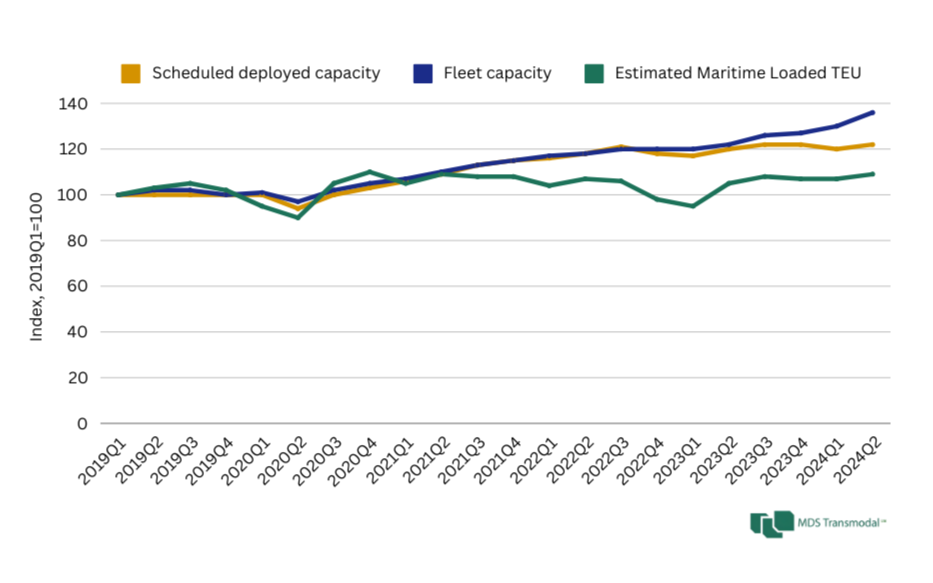

In 2024Q2, global deepsea fleet capacity (that is, capacity available to shipping lines) is estimated to have been 11.5% higher than in 2023Q2, reflecting the arrival of further new vessels into the market. During the same period, capacity scheduled to be deployed by the shipping lines (that is, capacity allocated by the shipping lines to trade lanes) has grown at a much slower rate of 1.8%.

As shown in the following graph, fleet capacity has been continually growing faster than scheduled deployed capacity since around 2022Q4, with the gap between the two enlarging.

Focusing on services that call at three or more ports on deepsea routes, thus excluding two-port rotations that do not typically constitute deepsea services, in this short article we will analyse how shipping lines are deploying their vessels, specifically whether they are pressing the accelerator on the hub-and-spoke model or if they are opting for more direct services. The comparison is drawn from a detailed analysis of our data on scheduled deployed capacity between July 2023 and July 2024.

Fleet capacity vs scheduled deployed capacity

Fleet capacity refers to the total volume that a shipping company can deploy, while scheduled deployed capacity refers to the volume actually in service. The distinction becomes crucial when considering service frequency and routing. For instance, two ships with a combined fleet capacity of 2,000 teu can generate a scheduled deployed capacity of 52,000 teu if they operate on a weekly service. An increase in fleet capacity, such as adding three more ships, raises the fleet capacity to 5,000 teu without necessarily altering the scheduled capacity, highlighting the importance of vessel utilisation efficiency.

One significant trend observed over the past year is the lengthening of journey times (mainly caused by re-routing via the Cape of Good Hope away from the Bab al-Mandeb Strait) alongside a reduction in the number of ports in the rotation. This shift raises the question: is this due to a preference for a hub-and-spoke model or a pivot towards more direct services?

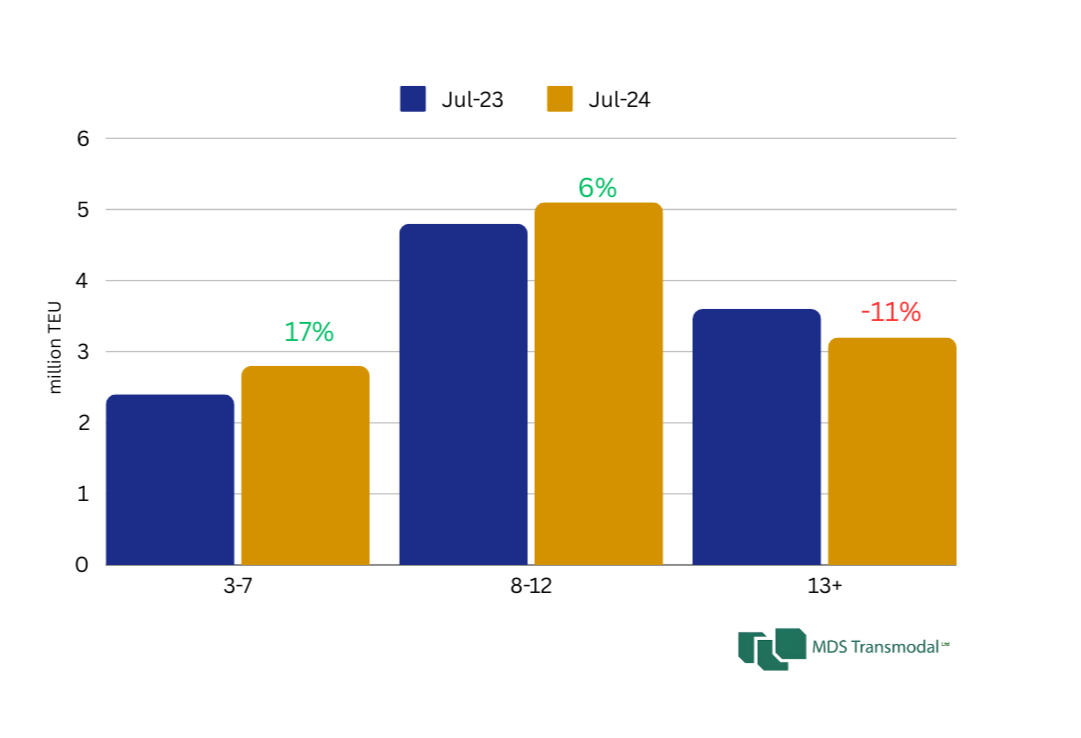

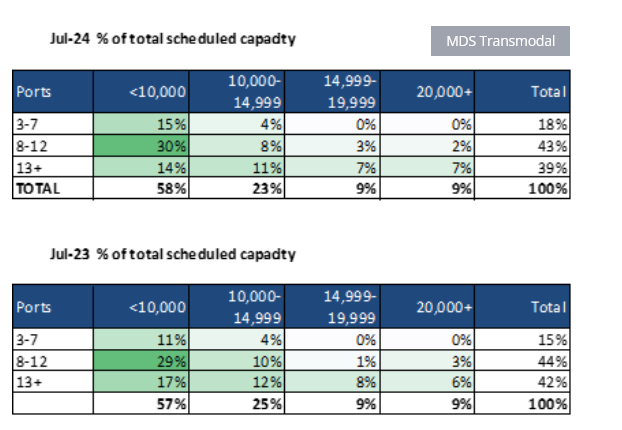

A comparative analysis of capacity deployed by the number of ports in rotation from July 2023 to July 2024 (chart above) reveals some critical changes:

- for the rotations calling at 3-7 ports, there was a 17% increase in capacity, rising from 2.4m teu to 2.8m teu, now accounting for 25% of total capacity (up from 22%);

- the rotations involving 8-12 ports saw a 6% increase in capacity, from 4.8m teu to 5.1m teu, now accounting for 46% of total capacity (up from 44%);

- however, rotations with 13 or more ports experienced an 11% decrease in capacity, from 3.6m teu to 3.2m teu, now accounting for 29% of total capacity (down from 33%).

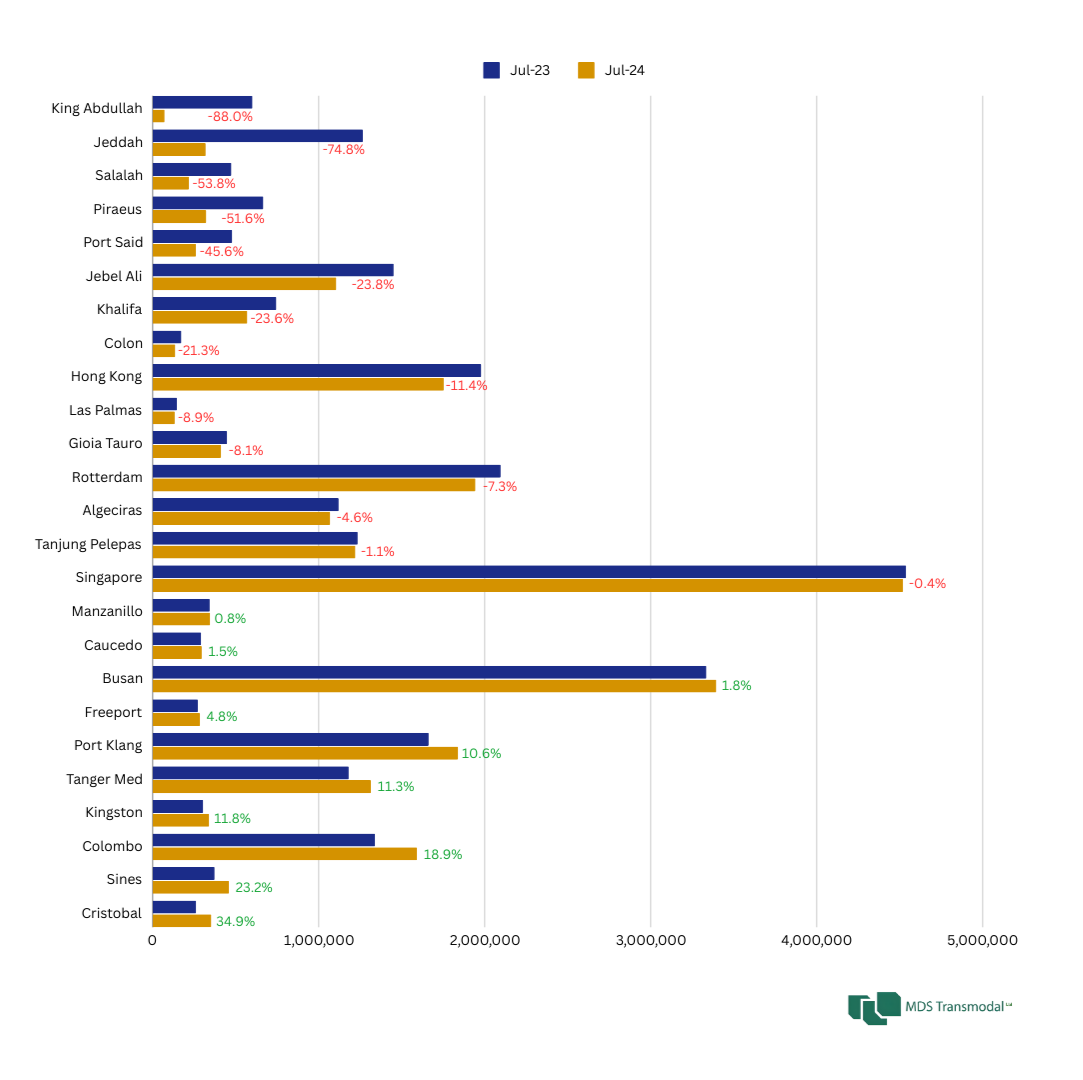

Drilling down the analysis to the port level, the capacity deployed on 25 key global hubs[1] provides a telling insight: the number of hubs experiencing an increase in capacity is lower than the number of hubs seeing a decline in capacity offered.

Extending the analysis to predominately gateway ports and focusing on ports with a capacity of over 0.5 million teu in July 2024, our data suggests that hub-and-spoke models are not prevailing; instead, there is a shift towards direct services, as they often utilise smaller vessels offering a more resilient option compared to the larger vessels typically associated with hub-and-spoke networks.

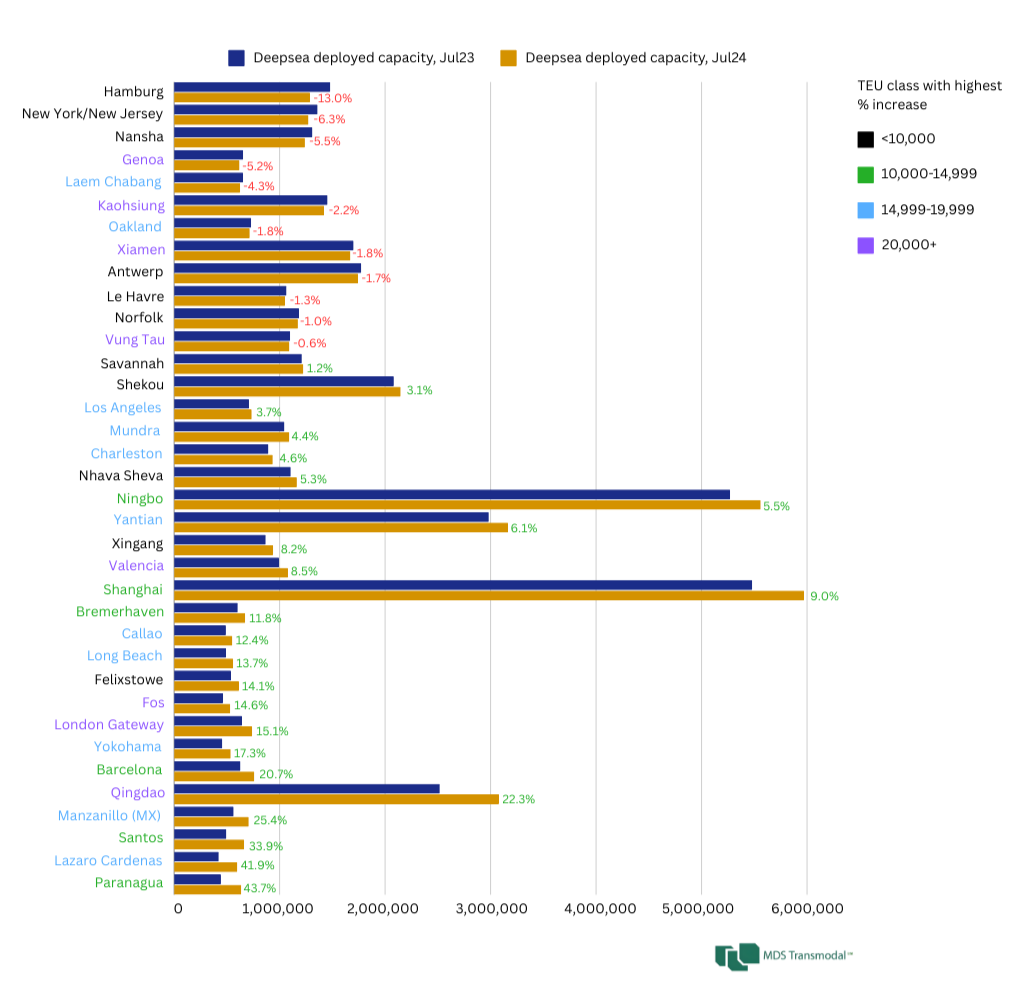

Further confirmation of the hub-and-spoke model being 'on pause' can be found in the deployment trends of vessels. Ships under 15,000 TEU are increasingly accounting for a larger proportion of capacity in shorter rotations compared to their larger counterparts. This trend underscores the industry's shift towards servicing non-hub ports[2] more frequently, enhancing the efficiency and directness of their operations.

The data from the past year indicates a trend towards direct services in deepsea shipping, with a notable ‘pause’ on the hub-and-spoke model. The resilience of smaller vessels and the strategic deployment of capacity towards non-hub ports highlights the industry’s adaptive strategies in response to evolving market demands in the context of the ongoing Red Sea crisis.

As the industry continues to navigate these changes, the balance between efficiency, frequency, and direct services will likely remain a focal point for shipping companies worldwide.

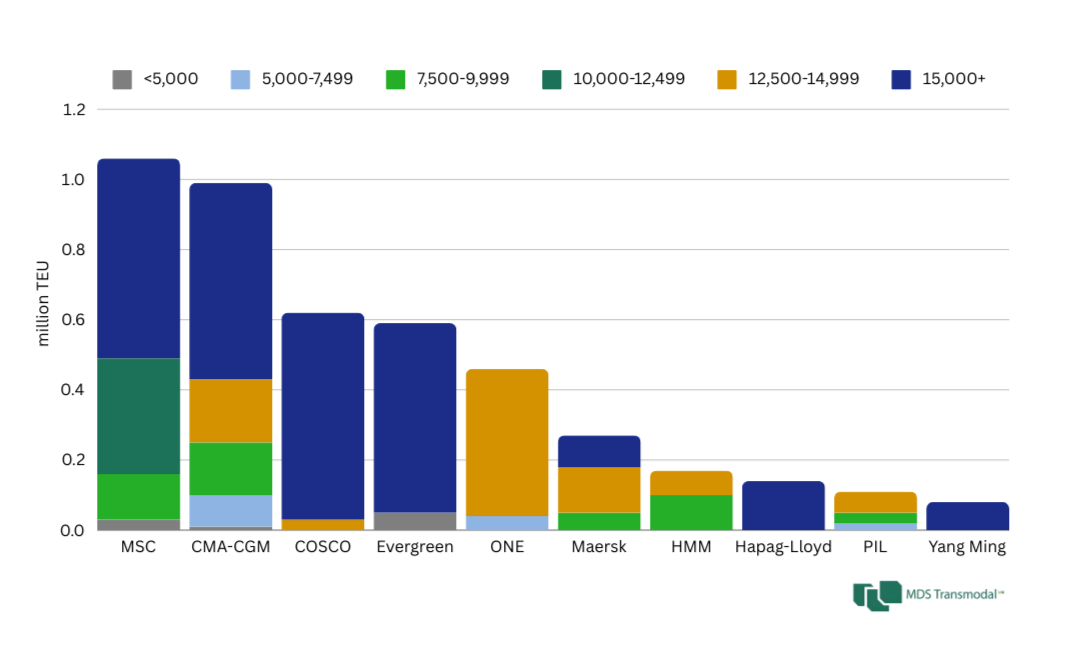

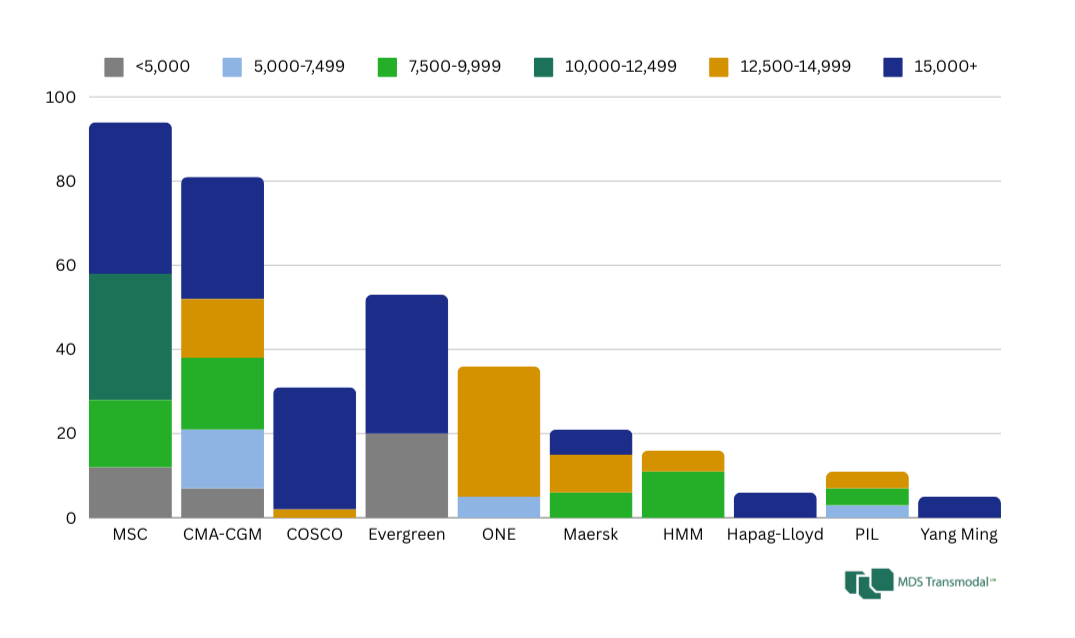

Looking ahead, the composition of the ships that MSC has on order is interesting: nearly half of the capacity expected to be delivered to the number one shipping line will comprise ships of under 12,500 teu, reflecting a strategic preference for flexibility and resilience (Figure 5). Looking at the number of ships, the percentage increases to 62%, Figure 6.