Network Reconfiguration Around the Indian Sub-Continent

The latest data for our Containership Databank for June 2026 points to a further acceleration in the strategic repositioning of deepsea container networks around the Indian Sub-Continent (ISC). What initially appeared to be a tactical response to disruption in the Red Sea and wider Middle East has increasingly evolved into a broader restructuring of liner network architecture, with the ISC emerging as a key organising hub within global east-west and north-south trade systems.

Between February and June 2026, monthly deepsea scheduled capacity passing via the ISC (excluding the Red Sea and Arabian Gulf) increased from 2.19 million TEU to 2.66 million TEU, representing growth of almost 21%. Compared with June 2025, capacity is now around 12% higher. At the same time, the number of deepsea services routed through the region increased from 104 to 127 between February and June 2026, further reinforcing the extent to which carriers are redesigning network structures around the ISC.

This growth is particularly significant because it is not simply driven by incremental demand. Instead, it reflects a more structural reconfiguration of service patterns. Carriers appear to be using the ISC increasingly as a flexible transhipment and redistribution platform capable of linking multiple long-haul corridors while also providing optionality under conditions of geopolitical uncertainty. A notable feature of the latest data is the growing concentration of capacity around strategic ports, particularly Colombo, Mundra and Nhava Sheva, which now account for a substantial share of total ISC deepsea capacity and service deployment.

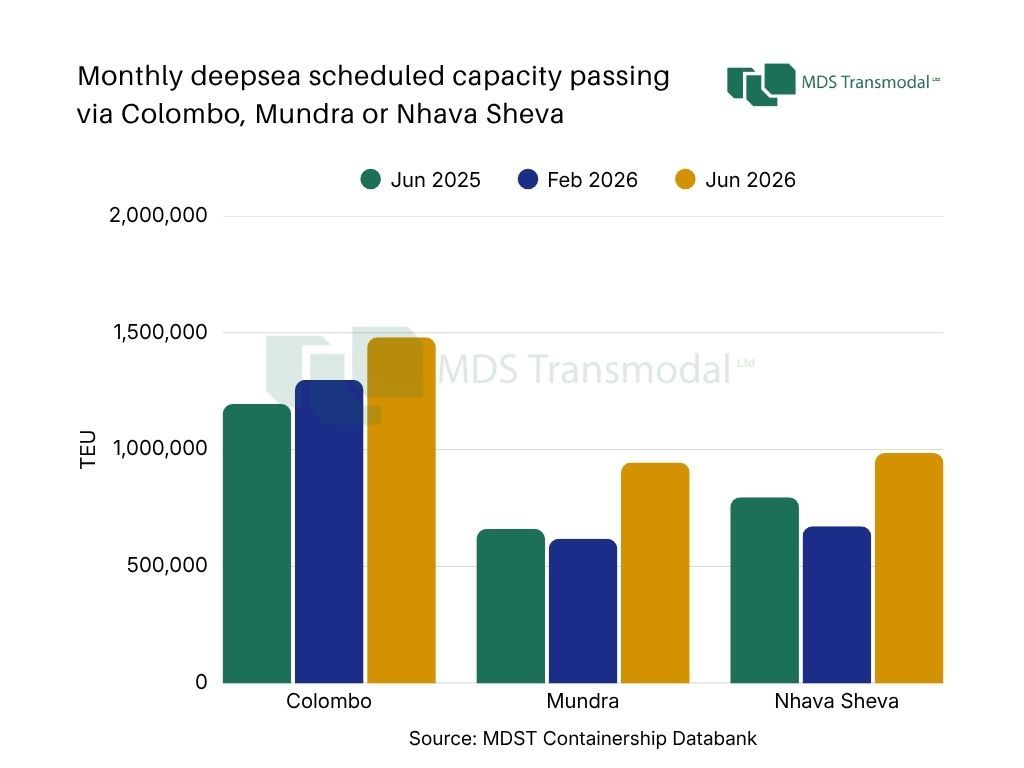

Colombo continues to consolidate its role as the region’s dominant transhipment hub. Excluding the capacity on the Red Sea and Arabian Gulf, deepsea capacity routed via Colombo increased from 1.30 million TEU in February 2026 to 1.48 million TEU in June 2026, an increase of 14%, while the number of services rose from 39 to 48. Colombo alone now handles approximately 56% of all ISC deepsea capacity captured in the dataset, underlining its pivotal role in maintaining connectivity across Asia-Europe, Asia-Africa and Asia-Americas corridors. The port’s scale, transhipment orientation and central geographic position continue to make it highly attractive for carriers seeking flexibility in network deployment and cargo redistribution.

The most striking developments are visible in the Indian gateways themselves. Mundra recorded exceptionally strong growth, with scheduled capacity increasing by 53% between February and June 2026, rising from 618,000 TEU to almost 1.0 million TEU. The number of services calling at Mundra expanded even more sharply, increasing by 70% over the same period. Compared with June 2025, capacity is now 43% higher. Mundra’s share of overall ISC capacity has consequently risen from 28% in February to 36% in June 2026. This suggests that carriers are increasingly integrating western Indian gateways directly into long-haul network structures rather than relying solely on traditional transhipment hubs.

A similar dynamic is emerging at Nhava Sheva, where capacity increased by 47% between February and June 2026, reaching almost 1 million TEU, while the number of services rose by 62%. On a year-on-year basis, capacity is up 24% and service deployment almost 40% higher. Nhava Sheva now accounts for approximately 37% of total ISC deepsea capacity within the dataset, compared with 31% only four months earlier.

Taken together, the data points to three interrelated developments.

First, carriers are clearly increasing their operational dependence on the ISC as an intermediate network fulcrum. Rather than functioning simply as an origin-destination region, the ISC is increasingly acting as a stitching point between multiple long-haul trade lanes. This is particularly important in the context of ongoing geopolitical disruption and persistent uncertainty surrounding traditional Middle Eastern routing structures.

Second, the expansion is becoming increasingly geographically diversified, with Indian ports becoming more deeply embedded into global service rotations. This reflects both sustained infrastructure development across the region and carriers’ broader strategy of increasing network flexibility through a wider set of complementary nodes, alongside the continued role of established transhipment hubs.

Third, the sharp increase in the number of services suggests that this is not merely a matter of upsizing existing loops. Instead, carriers appear to be introducing additional strings, alternative routings and more modular network structures capable of adapting quickly to changing operational conditions. This aligns with the broader industry trend away from highly optimised but vulnerable single-corridor systems towards more flexible and risk-diversified configurations.

Importantly, this does not necessarily imply a permanent displacement of the Middle East as a major network hub. However, it does suggest that the ISC has gained strategic importance in a way that may endure even if geopolitical conditions eventually stabilise. Previous experience following the Houthi-related disruption in the Red Sea demonstrated that network reconfigurations are slow and operationally complex to reverse. Once carriers establish new routings, commercial relationships and transhipment patterns, these structures often persist well beyond the initial disruption that triggered them.

As a result, the most likely medium-term outcome may not be a binary shift from the Middle East to the ISC, but rather the emergence of a more distributed and multi-nodal network model in which both regions coexist within a broader risk-diversified system. In that environment, the ISC (and particularly ports such as Colombo, Mundra and Nhava Sheva) could retain a structurally enhanced role within global liner shipping networks.