Reshaping capacity of global container shipping deployment

Analysis from MDST’s Containership Databank shows that restructuring of the global container shipping alliances is reshaping capacity deployment across the major East-West trades, with independent lines becoming more prominent.

A comparison of capacity deployment by container shipping lines from the MDST Contanership Databank between April 2026 and April 2025 highlights how carriers have adjusted network deployment following the introduction of the Gemini Cooperation and the Premier Alliance. While overall capacity trends vary by trade lane, a common theme is the growing importance of capacity deployed outside the major alliance structures.

Across the three east-west corridors analysed (Europe-North America, Far East-Europe and Far East-North America) capacity operated by carriers outside the main alliances (including MSC on its own) increased in relative importance, although with differences between trades.

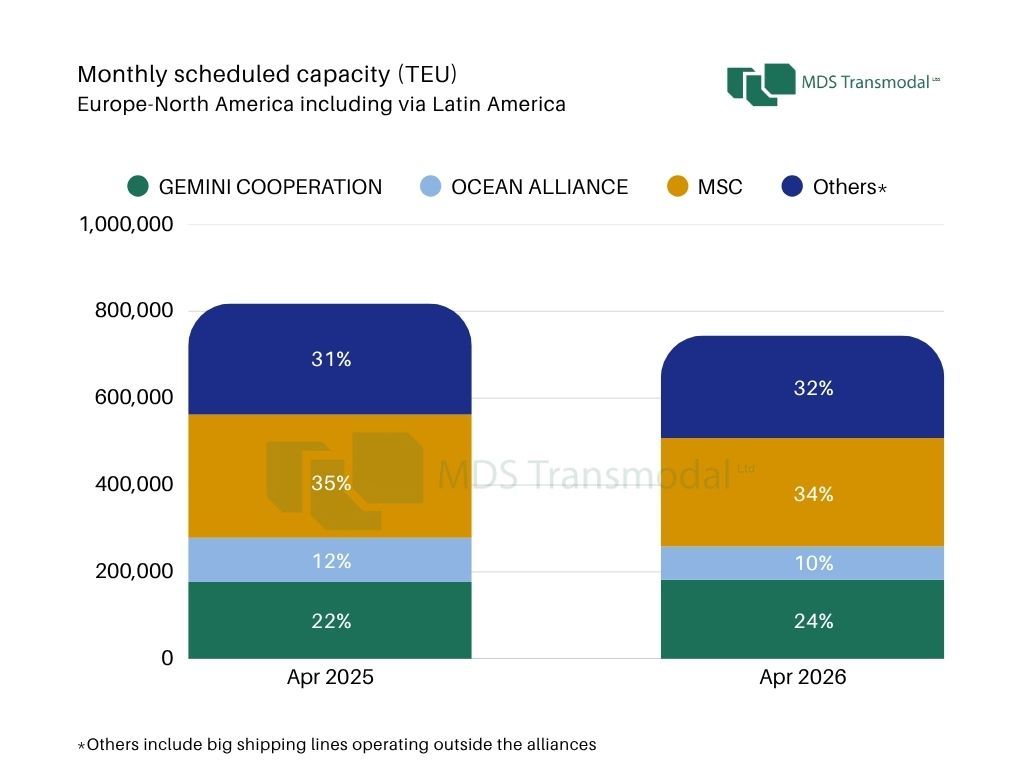

Europe-North America: a contracting market with Gemini gaining share

The Europe-North America trade corridor was the only corridor to record an overall decline in capacity. Total scheduled capacity fell by around 9% year-on-year, reflecting a weaker market and a rationalisation of transatlantic networks. Against this backdrop, the Gemini Cooperation was the only major grouping to expand capacity, increasing deployment by almost 3% and raising its market share from 22% to 24%. By contrast, the Ocean Alliance reduced capacity by more than 24%, resulting in the largest market share loss among the major groupings.

MSC also reduced deployment by 12%, although it remained the single largest operator on the trade, accounting for approximately one-third of total capacity. Capacity operated outside the alliance structure declined modestly (-8%), but the "Others" category still represented nearly 30% of total market capacity. Unlike the other trade lanes, much of this segment from a capacity point of view was composed of standalone services operated by major carriers such as Maersk, Hapag-Lloyd, CMA CGM and ZIM, rather than by a large number of niche operators. ZIM remained the largest truly independent carrier on the trade through its ZCA service, while other independent operators included ACL, Eimskip, Arkas/Turkon, NIRINT and several specialised North Atlantic carriers.

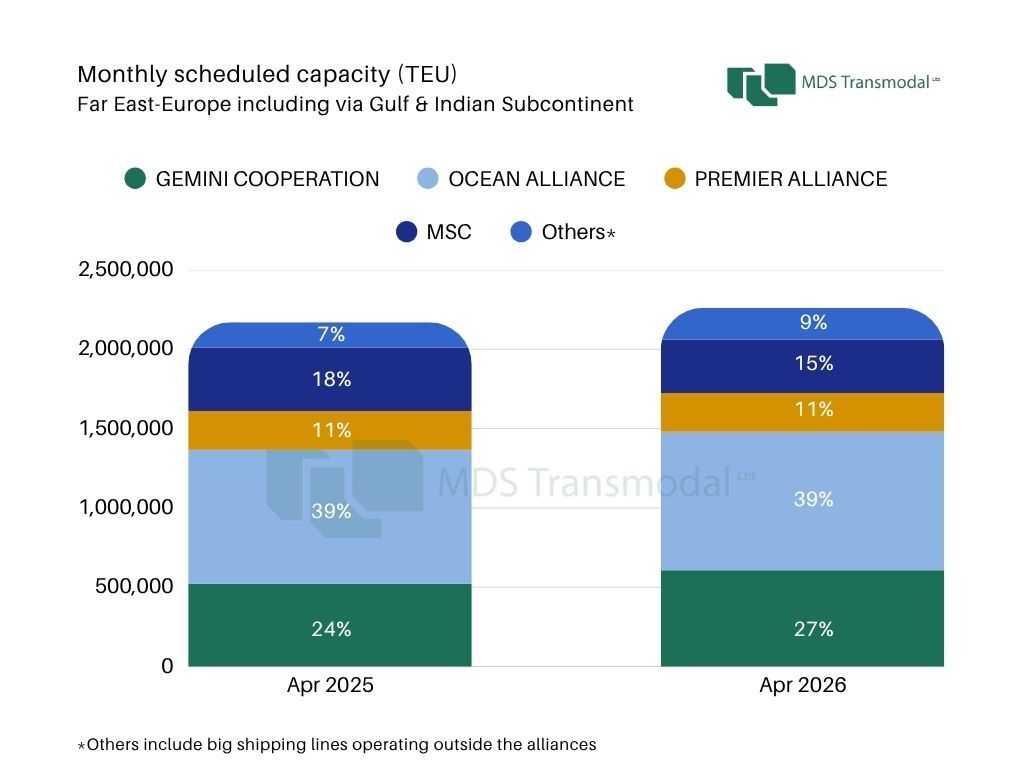

Far East-Europe & Med: Gemini expands while MSC retreats

The Far East–Europe & Med trade recorded moderate growth, with total capacity increasing by approximately 4%. Gemini was the clear winner among the major alliances, expanding capacity by more than 16% and increasing its market share from 24% to almost 27%. The Ocean Alliance remained the largest grouping and increased capacity modestly, while the Premier Alliance maintained a largely unchanged position. MSC moved in the opposite direction, reducing capacity by almost 16%, resulting in a decline in market share from 18% to 15%.

One of the most notable developments was the rapid growth of independent and non-alliance services. Capacity in the "Others" category increased by more than 25%, raising its market share from around 7% to almost 9%. This growth was driven by a combination of large carrier-operated services and emerging independent operators. HMM remained one of the largest non-alliance participants on the corridor, while ZIM expanded its ZMP service. Significant new capacity also came from CMA CGM's Ocean Rise Express and Wan Hai's FM1 service. The trade continues to exhibit a sizeable presence of Russian and Baltic-focused carriers operating outside traditional alliance networks, including FESCO, NewNew Shipping, Safetrans, OVP Shipping, Aurora Line - these operators have become an increasingly distinct feature of the Asia-Europe market since the restructuring of regional trade patterns.

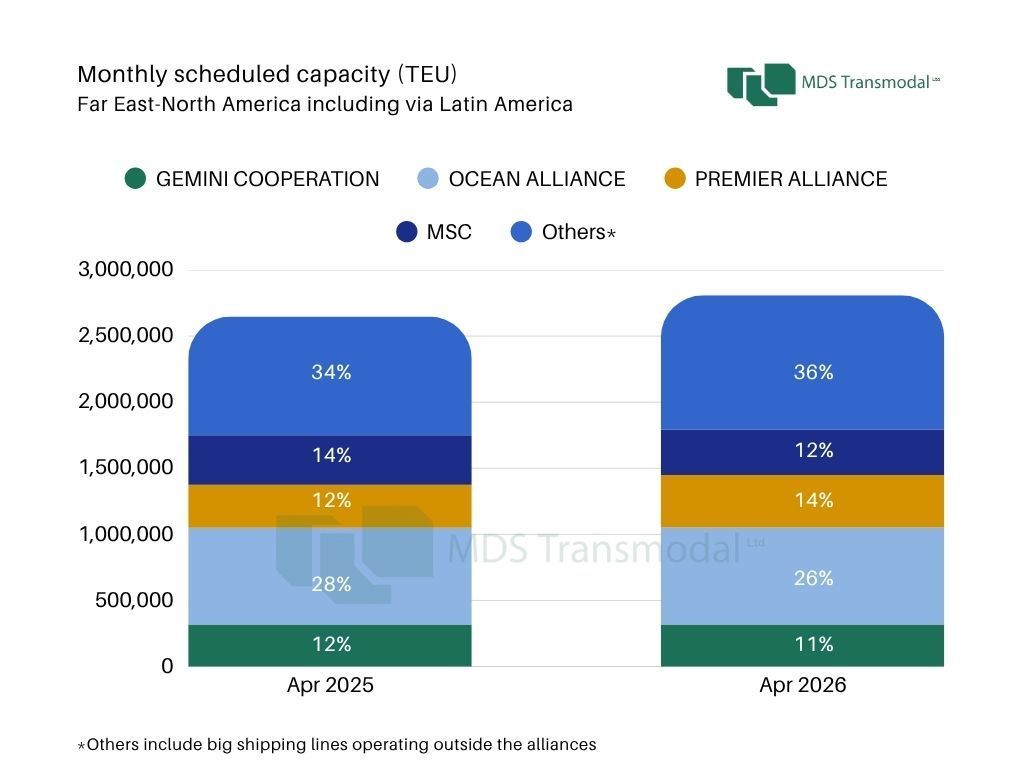

Far East-North America: independent operators drive market growth

The Far East-North America trade remains the most dynamic and fragmented of the three corridors analysed. Total capacity increased by approximately 6%, but the distribution of that growth was highly uneven. Ocean Alliance and Gemini maintained broadly stable capacity levels, while the Premier Alliance expanded deployment by more than 22%, making it the fastest-growing alliance grouping on the trade. MSC reduced capacity by approximately 8%, continuing the trend observed on the Asia-Europe corridor.

The most significant development was the expansion of the "Others" category, which grew by 13% to exceed one million TEU per month. Independent and non-alliance services accounted for roughly 70% of all market growth recorded between April 2025 and April 2026, increasing their share of total capacity from 34% to 36%. ZIM strengthened its position through growth across several transpacific services and a significant expansion of its cooperation with MSC on the Lone Star Express/ZSL service. Overall, ZIM remained the largest independent carrier outside MSC on the corridor. Growth outside the alliance system was supported by a broad range of operators, including CMA CGM, Maersk, COSCO, Hapag-Lloyd and HMM through standalone services, as well as medium-sized carriers such as SM Line, TS Lines, KMTC and Emirates Shipping Line.

Emerging themes across all three trades

Several common trends emerge from the analysis from the MDST Containership Databank. First, Gemini appears to be the principal beneficiary of the 2025 alliance restructuring. It increased market share on both the transatlantic and Asia–Europe corridors while maintaining a stable position on the transpacific trade.

Second, MSC reduced capacity across all three trade lanes. The declines were particularly pronounced on Far East-Europe and Europe-North America, suggesting a continued refinement of its standalone network strategy.

Third, the role of non-alliance services continues to expand. While alliances remain dominant on the major east–west trades, carriers are increasingly supplementing alliance networks with standalone services, cross-alliance arrangements and niche market offerings.

Finally, the degree of market fragmentation varies considerably by corridor. The transatlantic trade lane remains concentrated, with independent capacity largely controlled by a handful of major operators. The Far East-Europe trade lane exhibits growing diversification, driven by niche regional carriers and Russian-focused operators. Meanwhile, the Far East-North America trade has become the most fragmented market, with independent and non-alliance services now accounting for more than one-third of total deployed capacity and driving the majority of capacity growth.

Overall, the data from the Containership Databank suggests that the post-restructuring liner shipping market is not moving towards greater alliance dominance. Instead, while alliances remain central to network design, carriers are increasingly deploying capacity through a wider range of standalone and cooperative arrangements across the major east–west trades.